At Belardi Wong, we’ve built a database tracking billions of dollars in ecommerce revenue across channels and categories. For us, every client’s print and digital strategies are custom to their calendars and assortment, but macro trends matter! That’s why we track real-time performance across ad platforms, industries, and retailer types. Here is our recap of 2025!

Why does this matter?

Because strategy built in isolation is risky. Individual brand performance can feel unpredictable month to month, but when you zoom out across billions in ecommerce revenue and hundreds of retailers, patterns emerge. Understanding those patterns gives brands a competitive advantage. It allows you to anticipate shifts instead of reacting to them, invest in the right channels at the right time, and align product, promotion, and creative to how consumers are actually behaving. Our recap of 2025 is not just a look back. It is a roadmap for smarter decisions in 2026.

A Timeline View of the Year

Looking at 2025 quarter by quarter, the year was marked by resilience, volatility, and a steady shift toward value.

What We’re Seeing in the Data: YOY Performance Trends

When we look at YOY line graphs across ecommerce revenue, a few patterns stand out:

- Home Décor showed stronger momentum in 2025, with a mid-year lift and a meaningful rebound late in the year. Conversion strength helped offset softer session growth.

- Apparel, Shoes & Accessories remained steadier, but growth was more muted. Conversion rate softness was a consistent headwind throughout the year.

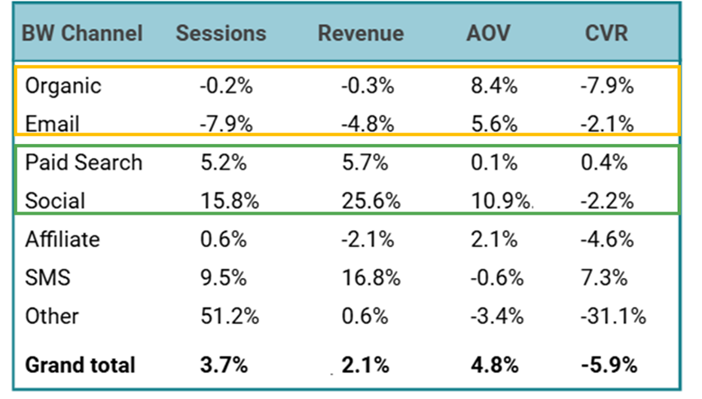

Channel performance also tells a clear story.

Ecommerce Performance by Last Click Channel Grouping 2025 vs. 2024

Social and SMS were growth drivers; Paid Search held relatively steady; and Email and Organic struggled under conversion pressure.

Category-Level Outcomes

Drilling into category graphs reveals where growth concentrated and where challenges persisted.

- Premium apparel brands (AOV over $250) outperformed, while lower-ticket categories faced more pressure.

- Emerging brands and brands targeting younger consumers posted the strongest gains, reinforcing the importance of audience alignment.

- Comfort footwear and high-ticket home furnishings lagged, reflecting more cautious discretionary spending.

- Brands with retail stores saw modest growth, highlighting more planned, purchase-driven store visits.

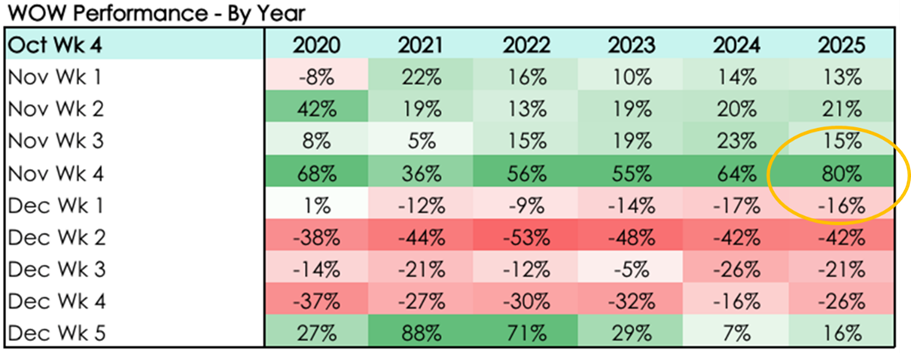

Holiday Build

Across categories, the message was consistent: performance favored brands with clear value propositions, strong products, and disciplined execution.

The week-by-week holiday timeline reinforces the year’s theme: shoppers were more intentional and value-driven – often delaying purchases until major deal moments, with the season’s biggest peaks concentrated around events like Cyber Week.

What This Means As We Plan for 2026

Brands that performed best in 2025 did not rely on single-channel wins or static plans. They measured frequently, adjusted quickly, and invested with intention across digital, direct mail, and CRM.

As we move into 2026, the opportunity is clear: use data to guide decisions, stay close to the customer, and remain flexible enough to pivot when conditions change.

Want to understand how these trends show up in your business? Connect with our team HERE to make sure your brand is positioned to capture demand during the busiest season of the year. For more insights follow us on LinkedIn HERE.